It is in the collective consciousness of Singaporeans that owning property is a big part of being – and getting – rich. For many families in Singapore, investing in property has proven to be a good way to preserve, if not enhance, their wealth and to build up a retirement nest egg. Veteran property consultant Tan Tiong Cheng, president of Knight Frank Asia Pacific, recalls that in the early 1970s, one could buy a freehold terrace house in the Siglap area for about S$25,000 to S$30,000; today you’d pay S$2.7 million to S$3 million for one. Similarly, a semi-detached house in the vicinity would have cost in the ballpark of S$35,000 to S$40,000 back then; today’s prices are S$4 million to S$4.5 million. “So in both cases, prices today are about 100 times what they were nearly five decades ago,” he said.

The Urban Redevelopment Authority’s benchmark overall private home price index in the second quarter of this year stood at 149 points, or 16.7 times the index reading of 8.9 points back in Q1 1975.

Land scarcity, Singapore’s phenomenal transformation from backwater to a global city that has created investor confidence, and the state’s pro-home ownership policies to give a sense of belonging to the nation have all fuelled growth in the city’s property prices.

The staggering rise in value has made this investment asset class compelling to Singaporeans. And then, of course, there is also the so-called Asian trait of wanting to acquire property to leave for the next generation.

As attractive as the returns from property have been, the capital appreciation from investing in the stockmarket can be even higher – depending on the timing of one’s entry and exit, of course.

Some analysts also opine that going forward, high rates of capital appreciation from property are not a sure thing, due to a host of reasons – including supply-demand dynamics.

Tight limits to the upside

Data supplied from Colliers International show that in the past 18 months or so, developers have bought so much land through both collective sales and state land tenders that the sites can generate about 40,000 private homes. According to BT’s back-of-the-envelope calculation based on the average annual developers’ sales of about 8,300 private homes for the 2014 to 2017 period, this would be equivalent to nearly five years’ supply.

Teh Hooi Ling, portfolio manager of Inclusif Value Fund, says: “There is no lack of supply. Demand is not likely to explode unless the government opens the gate wide to foreigners.”

She also reasons that with rental yield currently at near-historical lows, prices have stayed elevated because of low interest rates. When interest rates start to hike, prices may come under pressure. That will lift rental yield.

“The price appreciation that many of us are used to may not return,” says Ms Teh.

“The past 50 years have seen Singapore develop from a third world country to the first and then to a global city. It has reached that elevated level. Unless we allow unfettered capital and human inflow into Singapore, we are unlikely to see the slope of increase in real estate prices as experienced in the 1980s to mid-1990s. The more likely scenario is to see property prices rising in tandem with gross domestic product and money supply growth.”

Indeed, property industry players have been ruminating on the reason cited by the authorities in their decision in July to impose higher additional buyer’s stamp duty rates and lower loan-to-value limits, namely, “to cool the property market and keep price increases in line with economic fundamentals”.

JLL Singapore’s national director of research & consultancy Ong Teck Hui’s reading of that pronouncement is this: If upcycle property price increases are to be kept “in line with economic fundamentals”, then there is a likelihood of the market being interrupted by cooling measures during upcycles.

“If policy management of private home prices becomes a norm, the future rate of capital appreciation of private homes may be expected to decline.”

Holding property against equities

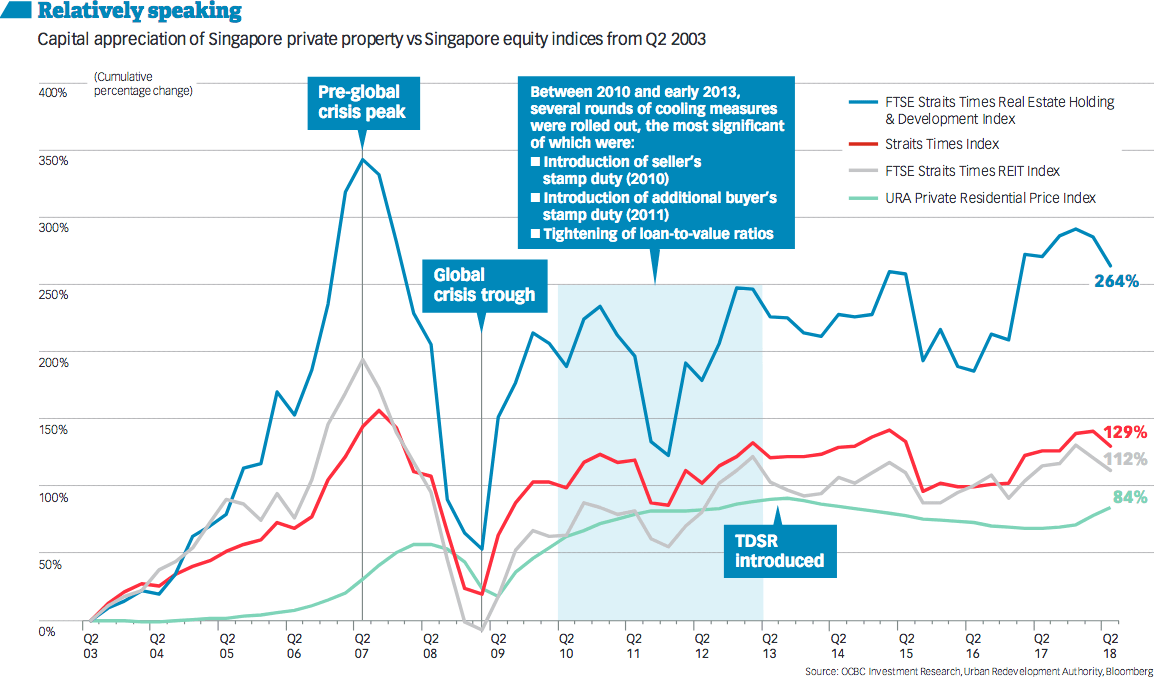

As things stand, the price appreciation of private homes in the past 15 years has been overshadowed by returns from investing in equities here – including property counters, an analysis by OCBC Investment Research investment analyst Andy Wong shows.

Between Q2 2003 and Q2 2018, the prices of physical private residential properties in Singapore as measured by the URA overall private home price index saw a cumulative increase of 84 per cent.

“On the other hand, investing in equities yielded a much stronger return. Based on price appreciation alone, the Straits Times Index (STI), FTSE Straits Times Real Estate Holding & Development Index (FSTREH) and FTSE Straits Times REIT Index (FSTREI) increased a whopping 129 per cent, 264 per cent and 112 per cent, respectively, during the same period.

“In fact, the FSTREH – which is a market capitalisation-weighted index that measures the performance of selected property holding and development companies listed on the mainboard of the Singapore Exchange – generated the highest capital appreciation for four out of the five periods (15-year, 10-year, 5-year, 2-year and 1-year) we tracked.”

In the one-year comparison, it was the URA private home price index that posted the biggest gain, reflecting the wave of bullish property market sentiment which culminated in the introduction of the cooling measures in July.

Mr Wong notes that “although investing in property stocks was the clear winner for four out of the five periods, investors should also take into consideration the potential risks and volatility of their investments”.

“If we look at the standard deviation of the returns from end-Q2 2003 to end-2Q 2018, this would be the lowest for the URA private home price index (0.33), followed by STI (0.39), FSTREI (0.41) and FSTREH (0.86).”

One can also take the analysis further by comparing the yields that investors would have received from the various asset classes. For investing in physical property, this would be the rental yield assuming the property is not owner-occupied. For equity investments, the additional return is derived from the dividend yield.

Net property yields tend to be lower than dividend yields.

Mr Wong’s analysis showed that for the period from Q2 2008 to Q2 2018, the annualised dividend yields averaged about 2.7 per cent for the FSTREH, 3.6 per cent for the STI and 6.4 per cent for the FSTREI during the same period.

Going by JLL data, the net yield for private apartments and condo units in prime districts averaged 2.24 per cent over the same period.

If we look at more recent data points, JLL’s net yield in Q2 2018 averaged 1.72 per cent, while OCBC’s analysis showed that the dividend yields were 3.0 per cent for the FSTREH, 4.0 per cent for the STI and 5.5 per cent for the FSTREI, as at end-June 2018.

Mr Wong concludes: “Hence, from a total returns basis, investing in Reits would have widened its attractiveness, compared to buying physical properties. Other factors that may support investing in equities over physical properties include liquidity and transaction costs,” he says.

Leverage, however, is what makes investing in physical property appealing. First-time buyers, for example, are allowed to borrow up to 75 per cent of the property valuation (assuming loan tenure is not more than 30 years and does not extend past the age of 65 for borrowers).

“Such high leverage is typically not available for normal retail investors in equity investments.”

The ownership psyche

So if one can reap higher returns from investing in other asset classes, and given the likelihood that prices of private homes are unlikely to escalate the way they have in the past, what makes folks here cling to physical property?

Ong Choon Fah, chief executive of Edmund Tie & Co, who lived in the US a few decades ago, makes this comparison. “In big countries, most people tend to rent as it gives them more flexibility to relocate to where their desired job is. So if you are in the US, you may have to move from coast to coast, from one city to another.

“When you are older and want to settle down and have a family, you may buy a home. But when you’re young, you may not have the means to buy a property and secondly, you are in your career trajectory, you chase jobs, your salary.

“On the other hand, Singapore is so small that you can reach any point within an hour; so you can buy a property in any part of the island. Moreover, we have the CPF savings system, which helps to defray your mortgage payments. And if you rent out your property, you benefit from having an additional source for covering your mortgage instalments.”

Ms Ong traces back the psyche here of wanting to own property to when Singapore became independent. “At that time, as a young nation how do you get people to have a stake in this country, how do you get people to sink their roots? One way is the home ownership policy to give people a sense of belonging; this is my country, this is my home. So you can start off with an HDB flat, then upgrade to a private condo and perhaps later even to a landed home.

“So it’s a combination of Singapore being small, the availability of financing through your CPF savings, and the government policy of encouraging home ownership – all these have made owning or investing in property so desirable.

“If you rent a house, if you want to push a nail into the wall, you’ll have to reinstate it when your lease ends. Whereas emotionally you feel more secure if you own your home and are free to do whatever you want. Nobody can boot you out. So most people here do not like the idea of renting.”

That said, Ms Ong argues that while Asians generally like to buy property, “if you actually do the calculations, forget the emotional ties, renting does make sense.”

For the investor, the potential gain – usually taken as a given – is what drives motivation.

“Residential yields are generally low, 1 to 2 per cent. However, the investor in each of us thinks that because Singapore is limited in size, land is scarce and with population growth, property prices must go up. So if you buy and sell at the right time, your total return can still be high. So you do not buy for the rental yield; you buy for the capital appreciation.”

A changing business model with policy risk

A seasoned property developer, who declined to be named, however, debunks this thinking. “It’s crazy. We should be looking at yields. We should not buy property at such low yields and then hope for capital appreciation. That is not following the fundamental principle of investing in real estate.”

He also highlights that the low interest rate environment in the past decade has distorted real estate markets all over the world.

“That is why governments have had to put in place cooling measures in one form or another, to cool real estate markets.”

Analysts note that some Singapore developers have changed their business model to rely less on the local residential property development business where margins have thinned, as the opportunities shift to where there is both greater upside and more stable recurring income.

The Singapore research head of an international property consulting group highlights the policy risks in the local market: “Because of the various rounds of cooling measures and because the Singapore housing market is being watched by the government, there is limited capital appreciation, so margins have thinned.”

One of the most dramatic transformation stories in business strategy is that of Ho Bee Land. It used to concentrate heavily on the Singapore residential property development business and has built more homes in the Sentosa Cove waterfront housing locale than any other developer.

Following the global crisis, the group moved to diversify its business and build up its recurring income base from investment property, which is a more sustainable model.

In 2010, Ho Bee bought a site next to Buona Vista MRT Interchange Station and developed it into The Metropolis, with 1.08 million sq ft of office space in two towers. The group also snapped up a string of completed office blocks in London in the past five years – the most recent being Ropemaker Place for which it completed the acquisition in June this year for £650 million (or S$1.16 billion based on the exchange rate at the time).

The second prong of Ho Bee’s diversification strategy has been to embark on overseas property development projects. In China, it has taken on mostly residential developments through joint ventures. Ho Bee has also developed a few residential projects in Australia. It has not bought any land for residential development in Singapore since the global crisis.

Roxy-Pacific Holdings, whose business used to be entirely in Singapore, has in the past five years ventured into overseas development projects in Kuala Lumpur and Sydney. It has also been increasing its recurring income by acquiring office buildings in Auckland and Melbourne as well as hotels in the Maldives, Osaka and Tokyo. The group is also developing a hotel in Phuket which is due to open at the end of 2019.

Chip Eng Seng, which is involved in the construction and Singapore residential property development business, has also been building up its recurring income through a series of hotel developments and acquisitions (in Singapore, Maldives, Perth and Adelaide) in recent years.

City Developments, whose stock is often seen as a proxy for investing in the Singapore residential sector, too, has set a 10-year target to grow its annual recurring earnings before interest, tax, depreciation and amortisation to S$900 million, from the nearly S$600 million last year. This is to help mitigate the volatility of the property development cycles.

With the smart money moving ahead with caution, perhaps potential buyers should take heed.

Adapted: BT

Join The Discussion