Purchasing a property in Singapore can be a daunting task, especially when it comes to financing. Whether you’re a first-time homebuyer or a seasoned property investor, understanding the financing options available to you is crucial to making the best decision for your financial future. In this guide, we’ll take a look at the different ways to finance a property purchase in Singapore, what to look out for when taking a loan, and how much you can expect to borrow based on your income.

Singapore’s property market is known for its stability and steady growth, making it an attractive destination for both local and foreign buyers. However, with property prices on the rise, obtaining a mortgage loan from a bank or financial institution is often necessary for most buyers.

Financing a property purchase involves obtaining a mortgage loan, which is a type of loan that is secured by the property you’re buying. The loan will be based on the value of the property and the borrower’s ability to repay the loan, as determined by the lender. This guide will provide an overview of the different aspects of financing a property purchase in Singapore, including the various loan options available, the down payment requirements, and other costs associated with buying a property.

Financing a property purchase in Singapore

The most common way to finance a property purchase in Singapore is through a mortgage loan from a bank or financial institution. A mortgage loan is a type of loan that is secured by the property you’re buying, meaning the lender will use the property as collateral in case you default on the loan.

When applying for a mortgage loan, the lender will typically require you to make a down payment of at least 25% of the property’s value. The lender will also assess your ability to repay the loan, based on your income and employment status. You will need to provide proof of income, such as your payslips and income tax statements, and at times proof of employment, such as an employment letter.

In addition to the down payment, you may also be required to purchase a mortgage insurance. Other costs associated with purchasing a property in Singapore include stamp duty and legal fees. Stamp duty is a tax that is imposed on the transfer of ownership of a property and is based on the property’s value. Legal fees are charges incurred for the services of a lawyer to handle the legal aspects of the property purchase.

It’s important to keep in mind that the terms and conditions of the loan may vary depending on the lender and the specific property. It’s always a good idea to consult with a financial advisor or bank representative to determine the best loan option for your situation.

What to look out for when taking a loan

When taking out a loan, it is important to consider the following factors to ensure that you’re getting the best deal possible:

- Interest rate: The interest rate will determine how much you will pay in addition to the principal amount of the loan. Look for a loan with the lowest interest rate you can qualify for.

- Repayment terms: Consider the length of time you will have to repay the loan and whether you can comfortably make the payments. Longer repayment terms may result in lower monthly payments, but the overall cost of the loan will be higher.

- Fees: Be aware of any additional fees such as origination fees, closing costs, or prepayment penalties. These fees can add up and significantly increase the overall cost of the loan.

- Flexibility: Consider whether the loan offers flexibility in terms of payment options, such as the ability to make extra payments or to change the due date of payments.

- Credit score: Be aware of your credit score and the minimum credit score required by the lender. A lower credit score may result in a higher interest rate and stricter terms.

- Fine print: Carefully review the terms and conditions of the loan, including the repayment schedule and any penalties for late or missed payments.

- Reputation: Before taking a loan from a lender, check the reputation of the lender. This can be done by searching for reviews or contacting the local regulatory body for information about the lender.

It’s important to carefully consider all of these factors and weigh the pros and cons of each loan offer before making a decision. Working with a financial advisor or bank representative can also help you to better understand the loan options available and find the best loan for your needs.

How much can you borrow to buy a residential property in Singapore

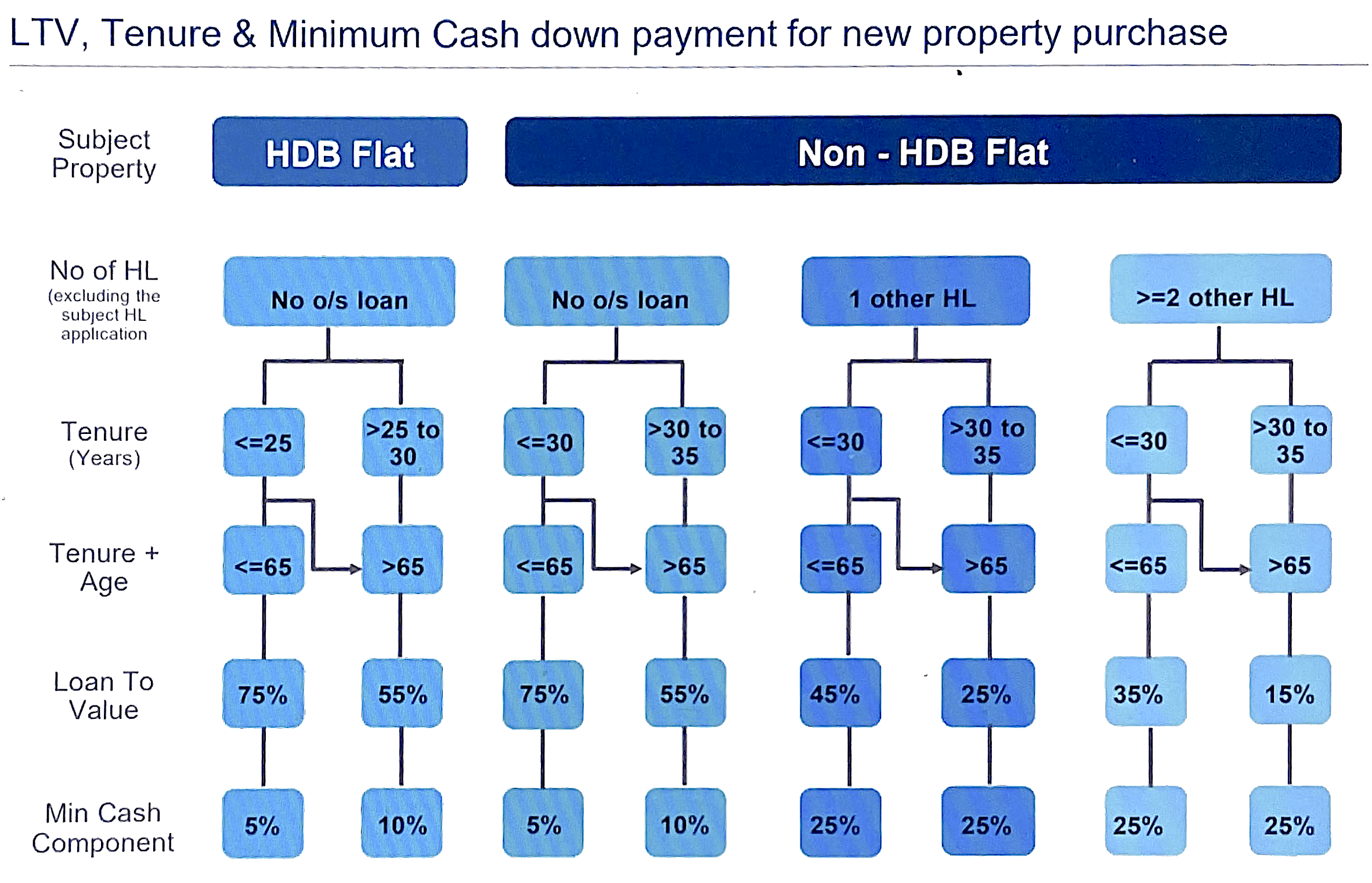

The amount you can borrow to buy a property in Singapore will depend on several factors, including your income, credit score, and debt-to-income ratio. Typically, most financial institutions in Singapore will allow you to borrow up to 75% of the property’s value or purchase price whichever lower, but this can vary depending on the lender and your financial situation.

To calculate the maximum loan amount you can borrow, most banks in Singapore use the Total Debt Servicing Ratio (TDSR) framework. The TDSR framework limits the amount of debt an individual can take on based on their income. The TDSR framework states that a borrower’s total monthly debt repayment obligations should not exceed 55% of his gross monthly income.

Additionally, the Monetary Authority of Singapore (MAS) has implemented the Loan-To-Value (LTV) framework, which limits the amount of loan you can take based on the value of the property you’re buying. LTV is the proportion of the property value that you can finance through a loan.

It’s important to note that these are the general guidelines and the actual amount you can borrow may vary depending on your individual financial situation and the lender’s requirements. It’s always a good idea to consult with a financial advisor or bank representative to determine the amount you can borrow based on your specific circumstances.

Conclusion

In conclusion, financing a property purchase in Singapore is a complex process that requires careful consideration of various factors such as income, credit score, and debt-to-income ratio. It’s essential to understand the different loan options available, the down payment requirements, and other costs associated with buying a property. It’s also important to consider the terms and conditions of the loan, including the interest rate, repayment terms, and any additional fees.

When looking for a home loan, it’s important to shop around and compare the different loan options offered by different banks. Some of the popular banks for home loans in Singapore include DBS Bank, OCBC Bank, United Overseas Bank (UOB), Maybank, Standard Chartered Bank, and Citibank.

It’s important to note that the terms and conditions of the loan may vary depending on the lender, the type of property you’re buying, and your individual financial situation. Additionally, the best bank for home loan can change over time, it’s always a good idea to check with the financial institution or bank representative to confirm the current offers before making a property purchase.

If you have any further questions or need more information about financing a property purchase in Singapore, it is always a good idea to consult with a financial advisor or bank representative to determine the best loan option for your situation. They will be able to provide expert advice and guidance on the financing process. Remember that purchasing a property is a significant financial commitment and it’s essential to make an informed decision that’s best for your financial future.

Join The Discussion